Bet the Tailwind, Not the Brand

Intel is up 281% in six months. I read every bull case at the bottom and passed on all of them.

The pieces were on X and Substack a few months ago, making the Intel-as-AI-proxy argument. Intel had been one of the worst performers in the sector. Management was visibly trying to find a story. Earnings calls sounded like a company that hadn’t found its footing. I stress-tested the thesis against the GPU narrative. Nvidia had won training decisively. Gaudi wasn’t gaining traction. The data centre business was struggling. It failed the test. I moved on.

Then I read Ben Thompson on the last earnings call and realised what I had missed.

I had the right company in my head. I didn’t have the gate.

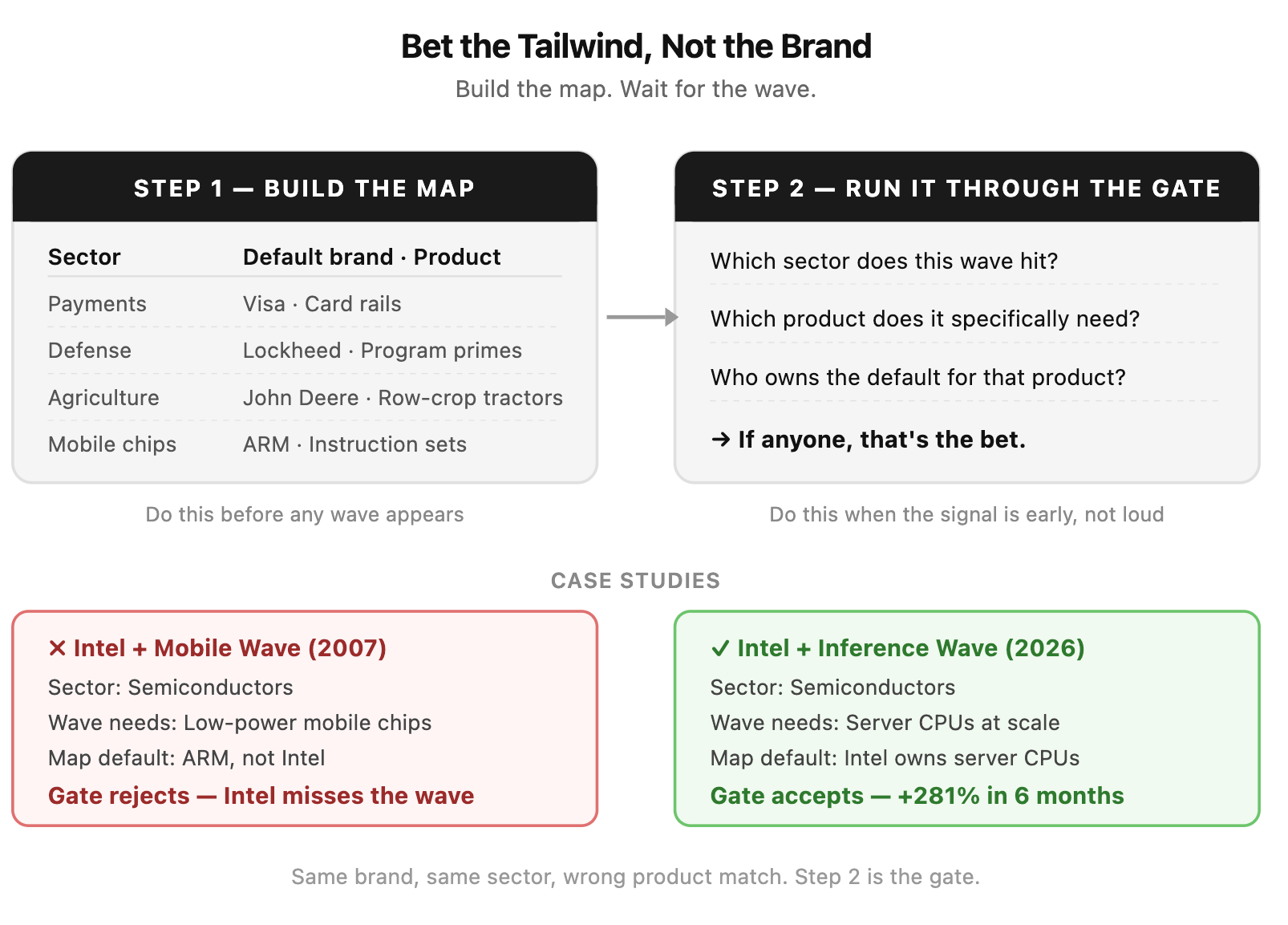

The gate is easier to see when it rejects. Run it on 2007.

Mobile was forming. The most recognised chip brand in the world was Intel. If I had stopped at “find the trusted brand in semis,” I’d have bought Intel. I’d have lost.

Mobile needed low-power chips that ran inside a phone. That wasn’t Intel’s product. ARM and Qualcomm owned it. Intel’s CPU trust was real and it didn’t transfer. The tailwind needed something different.

Same sector, same trusted brand, wrong product match. That’s the gate.

My first instinct is always to ask: who is the trusted brand here? The harder question, the one that actually pays, is: does what they make match what this wave needs?

Now 2026. Same gate, different outcome.

Intel is still the default for server CPUs. “Default” is the right word here, not “trust.” Hyperscalers don’t re-evaluate server CPU vendors from scratch every cycle. There are validated reference designs, qualified SKUs, procurement defaults, a decade of certifications, BIOS and firmware integration paths that just exist. When demand for the category spikes, the default vendor catches most of it before anyone runs a fresh RFP. That’s the asset. Brand-as-default-in-the-procurement-flow, not brand-as-vibe.

The AI wave is no longer just a training story. As inference scales, a real chunk of the load runs on CPUs: embeddings, retrieval, smaller-model serving, recommender systems, the long tail that doesn’t fit on a hot GPU. Most LLM inference still runs on accelerators. But enough of it is CPU-bound that server CPU demand re-rated.

Run it through the gate. Tailwind: inference scaling. Product the wave needs: server CPUs. Who owns the procurement default for server CPUs: Intel.

The bet was sitting there in January. I was evaluating Intel from scratch (GPU miss, uncertain management, bad recent performance) instead of running it through the gate I didn’t have yet.

So the framework, sharper.

Step one: build a map of who is the default in each category, and the precise product they are the default for. Not which brand I recognise. Which brand the buyer doesn’t bother re-evaluating, and the specific product that holds that status. Visa: card payment rails. Lockheed Martin: prime contractor on major US defense programs. John Deere: row-crop tractors and combines. ARM: low-power instruction sets. The map is sector × product × who-owns-the-default, and building it is most of the work.

Step two: when a tailwind forms, run it through the gate. Does this wave need a product where someone on the map already owns the default? If yes, that’s the bet. If the trusted brand exists but the product doesn’t match (Intel and mobile in 2007), the gate kills it.

Building the map before the tailwind is loud is the entire point. By the time X and Substack are writing about it, the move has already happened.

I had Intel in my head in January. I didn’t have the map. That cost me the trade.